Welcome to coveredcallETFs.com. CoveredcallETFs.com is built to be a gateway that offers an introduction to Covered Call ETFs, how they work and which benefits they offer. ETFs are a relatively new type of investment that gives you the chance to use investment strategies previously only available to big hedge funds and investment banks due to the high cost associated with replicating these strategies. ETFs are now available to regular investors in the United States and Canada as well as a number of other countries. This offers small retail and institutional investors the chance to earn a good return on invested capital in slow-moving or falling markets.

Here are some of the questions we answer on this website:

Whether you should sell your ETFs or borrow money for the down payment of a house. Where to check the interest rates in local markets such as the UK and Sweden.

If Covered call ETF:s are a good investment in your country. Local laws and tax regulations can have a huge impact on which investments you should make. An investment that is good if you live in Sweden or the UK can be horrible if you live in the US.

What is an ETF (Exchange-Traded Fund)?

If you’re new to investing, you’ve probably heard the term ETF thrown around a lot. ETFs are one of those financial tools that sound way more complicated than they really are. So let’s break it down in plain English.

The acronym ETF stands for Exchange-Traded Fund. It is very similar to a mutual fund, but the fund shares are listed on an exchange and traded in a manner very similar to stock trading. While shares of a standard mutual fund are normally only bought and sold once a day, the shares of an ETF are bought and sold continuously throughout the trading day. That means you can buy or sell shares in an ETF throughout the day using a regular brokerage account.

A mutual fund or exchange-traded fund is essentially a bundle of investments. Instead of you picking individual assets (eg. stocks) you buy shares in a fund. The fund takes the money from all the share owners and use it to invest. A big advantage with using funds is that you get instant diversification. Example: Let’s say you want to invest in tech companies. You could buy shares of Apple, Amazon, Microsoft, Google, and so on—one company for each purchase. But that’s time-consuming and pricey. Instead, you can buy shares in a tech-focused mutual fund or ETF, which already owns shares in all those companies.

This gives you diversification, which is a fancy way of saying you’re not putting all your eggs in one basket. If one company stumbles, the others can help balance it out. It’s less risky than betting everything on one stock. For a new investor with a small budget, achieving a proper degree of diversification buy investing in individual assets can be difficult. With mutual funds and ETFs, you can invest a small amount of money and get instant diversification.

Key Features of ETFs

Diversification: ETFs often track an index, such as the S&P 500 or NASDAQ-100, meaning when you buy shares of an ETF, you’re investing in a wide range of companies or assets. This diversification helps spread risk, as you’re not relying on the performance of a single stock or bond.

Trading Like a Stock: ETFs are bought and sold on stock exchanges throughout the trading day, just like individual stocks. This means their price fluctuates based on market supply and demand, unlike mutual funds, which are priced once daily after markets close.

Low Fees: ETFs tend to have lower expense ratios compared to mutual funds. Since many ETFs are passively managed (they simply track an index rather than relying on a fund manager to pick stocks), their operating costs are usually lower. Actively managed ETFs, however, tend to have higher fees.

Liquidity: Because ETFs are traded on exchanges, they are generally considered to be liquid, meaning you can buy or sell them easily during market hours. However, liquidity can vary depending on the ETF’s volume and the assets it holds.

Transparency: Most ETFs disclose their holdings on a daily basis, giving investors clear insight into where their money is invested. This transparency is one of the features that sets ETFs apart from mutual funds, which may only disclose holdings quarterly.

ETFs Are Available For Many Different Niches

Whatever you’re into—or whatever financial strategy you want to follow—you can probably find an ETF that will at least be close to what you want.

Here are a few examples:

ETFs that are designed to follow a stock index, e.g. the &P 500.

ETFs that invest in companies in specific industries, e.g. tech, healthcare, or energy.

ETFs that invest in bonds, or a combination of stocks and bonds.

ETFs that invest in real estate.

ETFs that are designed to follow a commodity price, or a basket of commodities.

ETFs that invest in specific geographical markets, e.g. South East Asia.

ETFs that invest in something very specific, e.g. renewable energy, gaming companies, or AI companies.

ETFs vs. Mutual Funds: What’s the Difference?

Both ETFs and mutual funds are collections of investments, but they work differently. ETFs trade like stocks, meaning you can buy and sell them any time during market hours. Mutual funds, on the other hand, only trade once per day, after the market closes.

ETFs usually have lower fees and more flexibility. That’s why they’re especially popular among beginner investors and people using DIY platforms like Robinhood, Fidelity, or Vanguard.

Why People Like ETFs

Low cost: Most ETFs have lower fees than mutual funds.

Easy access: You can invest in an entire market or sector in one move.(This is also possible with mutual funds.)

Transparency: You can usually see exactly what the ETF holds.

Flexibility: Buy or sell anytime during the trading day, just like a stock.

Good for beginners: You don’t need to be a stock-picking genius to get started.(This is also true for mutual funds.)

Diversification: Even if you only have a small amount of money to invest, you can achieve a high degree of diversification. (This is also true for mutual funds.)

How ETFs Work: Simple Mechanics Behind the Scenes

ETFs might look like mutual funds on the surface—they both let you invest in a collection of assets—but ETFs come with one major difference: they trade on stock exchanges in real time. That means you can buy and sell them just like regular stocks, whenever the market is open.

Here’s what that actually means in practice:

Real-Time Price Changes

With mutual funds, the price (called the NAV, or Net Asset Value) is set once per day after the market closes. So if you place an order at noon, you won’t know the exact price until later that evening. ETFs don’t work like that. Their prices move throughout the trading day—just like Apple, Tesla, or any other stock. If demand goes up, the price goes up. If there’s a sell-off, the price drops. You can watch the ticker change by the minute, which is great for people who like to keep an eye on market timing.

They Trade Like Stocks—With All the Tools That Come With It

ETFs are super accessible. You can buy them on just about any trading platform—Robinhood, Fidelity, E*TRADE, Charles Schwab, Vanguard, and more. If you have a brokerage account, you’re good to go. When you place an order, it goes through like any other stock. You can buy one fund share, ten, or even fractional fund shares depending on the platform.

Since ETFs behave like stocks, you can do a lot more than just buy and hold:

Set a limit order to buy only at a certain price

Use stop-loss orders to sell if the price dips below a set level

Short an ETF (if you think it’ll drop in value)

Hold long-term as a stable part of your investment strategy

Some investors trade ETFs daily. On the other end of the spectrum, we find the investors who buy ETF shares and hold on to them for years. How you use and ETF depends on your goals—but the flexibility is there.

In short, ETFs give you mutual fund-level diversity with stock-level control. You get access to a basket of investments, but with way more freedom in how you buy and sell the fund shares.

What is a covered call ETF?

An ETF is a type of fund that owns a specific type of assets. SPY is the worlds largest ETF. The fund buys the 500 stocks listed on the S&P500 index. The funds results mirror that of S&P500.

A covered call ETF works in a similar way but put out Call options to increase the yield the fund gets each year. This increase the yield the fund gets when the market is going down or stands still but limits the upside in a bull market.

Lets look at a possible example: An ETF fund buys 100 shares of Microsoft stock. These shares provide a dividend yield of 3.2%. A Covered Call ETF would increase this yield by putting out a sell option on these 100 shares. They then sell this call option for 1% of the share value. (The exact price they get for their call options can vary). This allows them to increase the yield from 3.2% to 4.2% completely risk-free.

The only downside is if the stock quickly increases in value during the maturity of the option. In this situation, the ETF will be forced to sell their shares for a price below market value when the option is exercised. This limits the upside. The ETF will still make money but not as much as it would have made if they hadn’t put out the call option.

This makes the Covered Call ETFs an investment that is suitable for most market conditions except for bull markets where a covered call ETF might produce a lower return than regular ETFs and other funds.

Covered call ETFs will in other words offer:

Limited upside

Higher income.

Types of ETFs

ETFs come in many different shapes and sizes. Some are broad and low-risk, others are niche and bold—but they all give you access to groups of investments in a single trade. Whether you’re building a long-term portfolio or trying to bet on a trend, there’s probably an ETF for it.

Here’s a look at some of the most popular types of ETFs and what they’re built for.

Index ETFs

These are the classic, most common ETFs out there. They track market indices like the S&P 500, FTSE100, or Dow Jones (DJIA). The goal here isn’t to beat the market—it’s to track the market. If you want simple, steady exposure to a wide range of top-performing companies, index ETFs can be a great choice. This is where a lot of beginners start.

Example: SPDR S&P 500 ETF Trust is one of the most popular ETFs and it tracks the S&P 500. When you buy it, you’re essentially betting on the performance of 500 of the biggest companies in the U.S.

Sector ETFs

If you believe a specific industry is about to take off—or want to balance your portfolio with exposure to certain sectors—these are the way to go. Sector ETFs let you invest in focused areas like tech, healthcare, finance, or energy without needing to pick individual companies.

Example: XLK targets tech stocks like Apple, Microsoft, and Nvidia. XLF covers financial giants like JPMorgan and Bank of America.

Bond ETFs

These ETFs make it easy to invest in fixed-income assets like government bonds or corporate bonds. Normally, buying individual bonds takes a lot of research (and sometimes high minimums). Bond ETFs simplify all of that by pooling a range of bonds into one place.

Some of the largest and most well-known bond ETFs track the Bloomberg U.S. Aggregate Bond Index, and index commonly known simply as “the Agg”. The Agg is comprised of over 10,000 United States-issued fixed-income securities, e.g. Treasury bonds, mortgage-backed securities (MBS), and investment-grade corporate debt. ETFs tracking the Agg are often used to add stability and income to a portfolio, especially during market volatility.

Examples: Two of the largest ETFs tracking the Agg are the iShares Core U.S. Aggregate Bond ETF (ticker: AGG) or the Vanguard Total Bond Market ETF (BND). At the time of writing, each of them hold around $125 billion in assets. They have comparatively low costs and are popular choices among investors looking for long-term stability and low fees.

Of course, bond-tracking ETFs does not have to be as “boring” as the Agg-tracking ones, and you can pick ETFs with a different approach if you want to spice things up and are willing to take on more risk. There are for instance ETFs that will invest in bonds issued by governments and/or corporations in emerging markets. Such bonds come with higher risks (including currency risk and political risk) and the interest rates will reflect this. Note: Many emerging-market bond ETFs mitigate the currency risk somewhat by hedging for currency fluctuations.

Other Debt ETFs

There are many ETFs that hold investment-grade bonds, but you can also go for ETFs that invest in other types of debt. There are for instance ETFs that invest in floating-rate loans issued to companies with below-investment-grade credit ratings. Typically, this will involve senior loans, which are secured by the borrower’s assets and rank higher than most other credits if there is an insolvency.

A fairly new invention are the ETFs that offer exposure to private credit through publicly traded vehicles such as business development companies (BDCs) and collateralized loan obligations (CLOs). They can be very high yield, but are of course also high risk. Previously, investing in this type of debt was out of reach for the average retail investor, but through an ETF you do not need to be an institution or high-net-worth individual to get exposure.

Thematic or Niche ETFs

These are for investors who want to lean into specific trends or ideas—whether it’s emerging technology, renewable energy, cannabis, or space exploration. Thematic ETFs are often built around concepts or industries that are comparatively small today but are expected to grow at lot. They’re more volatile, but they also come with the potential for big returns if the trend plays out.

Example: BOTZ focuses on robotics and AI companies. TAN is built around solar energy firms.

If you want to learn more, a good place to start is The Global Industry Classification Standard (GICS, which sorts companies into 11 different core sectors, and then further breaks those down into 24 industry groups, 69 industries, and 158 sub-industries. If you want to be specific when you invest in thematic ETFs, having a good understanding of the GICS can be a useful tool in your toolbox.

A type of ETF that has grown very popular in the last few years is the one that invest in the semiconductor industry, and the GICS has been helpful in clarifying for investors why they should take a closer look at this niche. Within the core sector Tech, the GICS identifies three primary industry groups: Software and Services, Technology Hardware and Equipment, and Semiconductors and Semiconductor Equipment. Semiconductors and Semiconductor Equipment is important and distinct enough to warrant a separate group, instead of being clumped together with other hardware. As you probably know already, semiconductors are utilized to control electrical signals in a wide range of devices, and lot of our everyday technology rely on them – including computers. In 2014-2024, the S&P Semiconductors Select Industry Index delivered an annualized return above 17%, which meant that it outpaced both the S&P Tech Hardware Index and the S&P Software & Services Index.

Examples of semiconductor ETFs:

Invesco PHLX Semiconductor ETF (SOXQ) Expense ratio 0.19%

SOXQ tracks the PHLX Semiconductor Sector Index, a benchmark that has been around since 1993. With an expense ratio of just 0.19%, SOXQ has become popular among long-term investors who wish to keep the costs down. The historical performance of SOXQ has been similar to that of VanEck Semiconductor ETF (SMH) and iShares Semiconductor ETF (SOXX), and there are big portfolio overlaps between these three ETFs.

VanEck Semiconductor ETF (SMH) Expense ratio 0.35%

VanEck Fabless Semiconductor ETF (SMHX) Expense ratio 0.35%

iShares Semiconductor ETF (SOXX) Expense ratio 0.35% SOXX tracks the NYSE Semiconductor Index. An options chain is available for investors who wish to buy or sell calls and puts. Note: There is a lot of exposure overlap between SOXX and SMH, but SOXX underweights NVDA and TSM.

SPDR S&P Semiconductor ETF (XSD) Expense ratio 0.35% XSD can be a good choice if you want exposure to up-and-coming companies instead of focusing on well-established giants. The XSD tracks the S&P Semiconductor Select Industry Index, and since this index is equal weighted, a smaller semiconductor firm that just made it into the index will have the same weighting as a giant whenever he index re-balances.

First Trust Nasdaq Semiconductor ETF (FTXL) Expense ratio 0.60%

Direxion Daily Semiconductor Bull 3x Shares (SOXL) Expense ratio 0.75% SOXL is a popular choice among day traders and swing traders, who are less concerned with the 0.75% expense ratio than buy-and-hold investors. SOXL does not prioritize low cost and high diversification – it is an ETF that brings the volatility sought after by short-term traders, and this has translated into high liquidity which is also what short-term traders need. SOXL is a so-called leveraged ETF, which uses derivatives to outperform an index. The goal for SOXL is to deliver a daily return of three times that of the NYSE Semiconductor Index, and the managers of SOXL are using index swaps to achieve this

International ETFs

Since a lot of the mainstream ETFs are heavily focused on the U.S. market, international ETFs have evolved to cater to investors who want exposure to other countries and regions around the globe.

International ETFs can give you exposure to different countries or regions without you needing to research individual foreign companies. Some are region-based (like Europe or Asia), while others are targeting specific emerging markets.

In this context, international simply tends to mean “not focused on the U.S.”, since the U.S. market is so dominant in the world of ETFs.

Example: EEM invests in emerging markets like China, Brazil, and India. VEU holds a mix of global stocks but leaves out U.S. companies.

Dividend ETFs

These ETFs focus on companies that regularly pay out dividends. They’re a solid choice for investors who want to generate consistent income—whether that’s to reinvest or help fund retirement. If stocks owned by the ETF pay dividends, the money is passed along to the investors. Most EFTs pay out the money quarterly on a pro-rata basis (how much you get depends on how many fund shares you own).

Example: VIG includes companies with a track record of growing their dividends over time. SCHD focuses on high-yield dividend stocks with strong fundamentals.

Benefits of ETFs: Why So Many Investors Choose Them

Pros and Cons of ETFs

Benefits of ETFs

Low Costs: Most ETFs, especially those that are passively managed, have lower fees than actively managed mutual funds.

Flexibility: ETFs can be traded throughout the day, allowing investors to react quickly to market conditions.

Tax Efficiency: ETFs are generally more tax-efficient than mutual funds because they don’t distribute capital gains to investors as frequently.

Accessibility: ETFs can be bought and sold through regular brokerage accounts, and you can invest in them with relatively small amounts of money, which makes them accessible to a wide range of investors.

ETFs have exploded in popularity over the last couple of decades—and it’s not just hype. They offer a smart, flexible, and cost-effective way to invest, whether you’re a beginner building your first portfolio or a seasoned investor looking to streamline things. So what exactly makes ETFs such a go-to option?

Here’s a breakdown of the biggest benefits that keep people coming back.

Diversification Without the Hassle

One of the best things about ETFs is that you get access to a broad range of investments with just a single purchase. Instead of buying dozens of individual stocks or bonds, you can buy one ETF that holds them all. This spreads out your risk—if one company in the ETF takes a hit, the others can help balance it out. It’s a simple way to avoid putting all your eggs in one basket, even with a small investment.

Of course, this can also be achieved using normal mutual funds.

Lower Fees That Don’t Eat Your Returns Most (but not all) ETFs are passively managed, which means they track an index rather than relying on a team of managers to pick stocks. That translates into lower costs for you. Mutual funds often come with higher expense ratios and sometimes even front-loaded fees. ETFs usually keep those expenses to a minimum, letting more of your money stay invested and working for you. With that said, index-tracking passively managed mutual funds with low fees are also available; the ETF is not the only way to go if you want to keep fund management fees down.

Buy and Sell Anytime (Just Like a Stock)

Unlike mutual funds which only trade once a day after the market closes, ETFs can be bought or sold any time the market is open. Want to make a move at 10 a.m.? No problem. Need to sell before closing? Go ahead. This kind of flexibility is a huge plus for people who like having more control over their timing.

Daily Transparency

Most ETFs disclose exactly what they hold every single day. That means you’re never left guessing where your money is actually going. Mutual funds, on the other hand, typically report holdings quarterly, which makes ETFs the more transparent option by far.

More Tax-Friendly Than Mutual Funds in the United States Thanks to something called the “in-kind redemption process” (don’t worry, you don’t need to memorize that), ETFs are usually more tax-efficient than mutual funds in the United States. In simple terms, when investors sell out of an ETF, it doesn’t trigger capital gains taxes for everyone else. That’s not always the case with mutual funds, which can hit you with unexpected tax bills—even if you didn’t sell anything.

ETFs vs. Mutual Funds vs. Stocks: What’s the Difference?

When you’re figuring out where to put your money, it can be tough to choose between ETFs, mutual funds, and individual stocks. Each one works a little differently, and they all come with their own pros and cons. Here’s a quick side-by-side breakdown to help make sense of it all—so you can pick what fits your investing style best.

Diversification

If you’re looking to spread out risk, both ETFs and mutual funds are solid picks. They pool your money across dozens or even hundreds of companies or assets, which lowers your exposure to any single one falling apart. Individual stocks, on the other hand, leave you riding the wave of one company’s performance—great if it pops, not so great if it tanks.

Of course, you can achieve diversification in your own stock portfolio by being mindful when you pick the stocks. Many beginners, however, start out with a small amount of money, and simply investing in 50+ different companies at the same time is not really feasible, unless you buy fractional shares. For a novice investor with $100 a month to invest, putting the money into a well diversified mutual fund or ETF is an easy way to ensure a high degree of diversification from day 1.

Note: Even though mutual funds and ETFs can be highly diversified, it is actually a good idea to employ some diversification when it comes to funds as well. As your portfolio grows, consider investing in several different funds instead of putting all your money into the same one.

Fees

ETFs win here. If you want to keep the fund fees down, passively managed ETFs are usually a great choice, as their fees tend to be much lower than what you would by mutual funds.

Mutual funds are more likely to be actively managed, and they also tend to come with sales charges and various maintenance costs baked in, which can pile on the costs. With that said, some of the passively managed index-tracking mutual funds have really low fees.

Individual stocks don’t come with ongoing fees.

Trading

ETFs and individual stocks are both traded throughout the day on stock exchanges. You can buy and sell them whenever the market’s open. Mutual funds? Not so much. You can only trade them once per day, after the market closes, and you won’t know the price until then.

Minimum Investment

ETFs and stocks are very beginner-friendly when it comes to getting started. Many platforms let you buy fractional shares, so you can invest with as little as $5 or $10. Mutual funds often require a higher minimum investment—sometimes $500, $1,000, or even more—depending on the fund.

Some stocks are not possible to purchase on a small budget unless you purchase a fractional share. The most famous example is BRK.A (Berkshire Hathaway Inc.), which – at the time of writing – has a share price of 750,000 USD. NVR is trading just below 7,560 USD, BKNG at 4,435 USD, and AZO just above 3,700 USD.

Which One Should You Pick?

Go with ETFs if you want easy diversification, low fees, and the ability to trade throughout the day.

Choose mutual funds if you’re more hands-off. Many people who invest in mutual funds want actively managed funds and are willing to pay the cost.

Try individual stocks if you enjoy researching companies, taking bigger risks, and potentially earning higher rewards—but with more volatility.

You can also mix and match. Many investors use a core of ETFs for stability, add mutual funds for certain managed strategies, and sprinkle in a few individual stocks for fun or growth potential. There’s no one-size-fits-all—just what fits you.

Feature

ETF

Mutual Fund

Individual Stocks

Diversification

High

High

Low (unless you own many)

Management Fees

Low

Medium to High

None

Traded Like a Stock

Yes

No

Yes

Minimum Investment

Very Low

Often High

Varies

Risks of Investing in ETFs: What to Watch Out For

Drawbacks of ETFs

Trading Fees: While ETFs generally have lower expense ratios, you may still have to pay a commission each time you buy or sell ETF shares, depending on your broker. Some brokers offer commission-free ETFs.

Market Risk: Like any investment tied to stocks or bonds, ETFs are subject to market volatility. If the index or sector the ETF tracks performs poorly, your investment will lose value.

Tracking Error: In some cases, an ETF may not perfectly match the performance of the index or assets it aims to replicate. This is known as tracking error.

ETFs are often praised for being easy, affordable, and beginner-friendly—but let’s not pretend they’re perfect. Like any investment, ETFs come with risks. Some are obvious, others sneak up on you if you’re not paying attention. Whether you’re new to the market or just building a more hands-on portfolio, it’s important to know what could go wrong before jumping in.

Market Risk: When the Whole Market Sinks, So Does Your ETF

Many ETFs follow a market index or sector. That’s great when things are going up—but if the market takes a dive, your ETF goes with it. Buying an S&P 500 ETF, for example, means you’re tied to the performance of the 500 largest U.S. companies. If the economy slows down, inflation spikes, or investor confidence tanks, expect your ETF’s value to drop too. Diversification helps spread risk, but it doesn’t erase it.

Liquidity Risk: Some ETFs Are Harder to Trade Than Others

Not all ETFs are created equal when it comes to trading volume. The big ones—like SPY or QQQ—trade millions of shares a day. But niche or thematic ETFs that focus on very specific industries or trends may barely move on some days. That’s a problem if you want to buy or sell fast, and it is also a problem for traders who want to use ETFs for day trading and aim to profit from small intraday movements. Thin trading volume can also lead to wider bid-ask spreads, meaning you might pay more or sell for less than you expected.

True Diversification vs. Apparent Diversification

It’s easy to assume that owning multiple ETFs gives you more protection. And while that’s true to a point, it can backfire. A lot of ETFs hold the same popular stocks—Apple, Microsoft, Amazon, Google—so buying five different ETFs might just mean you’re stacking up on the same names over and over. You think you’re diversified, but you’re still heavily exposed to the same companies. In order to achieve a higher degree of diversification, you need to be mindful when you decide which ETFs to invest in.

Hidden Costs: Beyond the Expense Ratio

ETFs are known for low fees, but there are other costs people forget. The bid-ask spread—the difference between what buyers are willing to pay and what sellers want—can eat into returns, especially with lower-volume ETFs. And then there’s the riskier side of the ETF world: leveraged ETFs. These are designed to multiply daily gains (or losses), and while they might look exciting, they’re volatile, expensive, and not meant for long-term holding.

How to Choose the Right ETF: A Practical Checklist

ETFs can make investing simple—but picking the right one? That takes a little thought. With thousands of ETFs out there, it’s easy to get overwhelmed or distracted by flashy names and trending themes. The good news? You don’t need to be a finance pro to make a smart pick. You just need to ask the right questions.

Here’s a straightforward checklist to help you cut through the noise and choose an ETF that actually fits your goals.

What Does the ETF Track?

Every ETF is built around something—an index, sector, trend, or group of assets. Start by looking at what the ETF is following. Is it a broad market index like the S&P 500? A specific industry like tech or healthcare? Or something more niche, like artificial intelligence or renewable energy?

If you’re aiming for long-term growth, broad market ETFs might be your go-to. If you want to play a specific trend, thematic ETFs could be worth a look. Just make sure the theme matches your market analysis and your risk tolerance.

How Much Does It Cost to Own?

Expense ratios are the ongoing fees you pay to keep the ETF in your portfolio. Lower is better, since each penny you pay in fees is a penny you can not invest and that will not give any returns for you. Always check the ratio before you buy. If it’s high, there better be a really good reason. Make sure the higher fee is really worth it in terms of growth compared to similar ETFs with lower fees.

Most of the well-known ETFs from major issuers have expense ratios under 0.20%. Some go as low as 0.03%. That difference may not sound like a big deal, but over time, higher fees eat into your returns—especially if you’re investing for the long haul. An ETF having an unusually high fee that is not made up for in returns can also make the fund shares less attractive on the share market.

Who’s Behind the ETF?

It is generally considered safer to stock with well-known issuers with a good track record. Big names like Vanguard, iShares (by BlackRock), and SPDR (by State Street) are known for reliability and solid fund management. If you’re looking at an ETF from a company you’ve never heard of, dig deeper before you make any decision. What’s their track record? Are they well-regarded in the investing world?

Trust matters when your money’s on the line.

Note: Since ETFs are listed on an exchange, you will get some additional safety. A reputable exchange will require a lot of paper work before any fund is permitted to be listed, and there are also ongoing requirements that must be fulfilled for the fund to stay listed.

What’s the Performance History?

Past performance isn’t everything—but it is something. Look at how the ETF has performed over the last 1, 3, and 5 years. Compare it to similar ETFs or its underlying index. Is it doing what it’s supposed to do? Does it move how you’d expect based on market conditions?

Don’t chase past returns, but do pay attention to consistency. Past returns do not guarantee future performances, but they can be an indication.

Does It Match Your Strategy?

Finally, ask yourself what you actually want from this investment. Are you looking for growth over the next 10–20 years? Steady income through dividends? Short-term exposure to a specific sector? Something to hedge against risk? Make sure the ETF lines up with your time horizon, risk tolerance, and overall plan. If you’re building a core portfolio, a volatile niche ETF probably isn’t the best fit. If you’re trying to add some spice to an otherwise boring setup, then maybe it is.

Tips for ETF Investors: How to Build Smarter, Stronger Portfolios

ETFs make it easy to start investing—but if you want to go from “just getting started” to building real wealth, it pays to be strategic. A few smart moves (and a few things to avoid) can help you get more out of every dollar you invest.

Here are some no-nonsense tips for making ETFs work harder for you.

Start With Broad ETFs First If you’re new to investing, don’t overthink it—begin with a broad-market ETF like VTI (which tracks the total U.S. stock market) or VOO (which tracks the S&P 500). These give you instant exposure to hundreds of companies across different sectors, all in one purchase. They’re low-cost, time-tested, and take the guesswork out of “what stock should I buy?”

Once you’ve built a solid foundation, then you can explore sector-specific or thematic ETFs if you want to add some variety.

Reinvest Dividends Automatically

If your ETF pays dividends, don’t just let the cash sit in your account. Turn on DRIP (Dividend Reinvestment Plan) through your broker if available. This automatically reinvests dividends back into more shares of the ETF, helping you build wealth through compounding over time.

Even small dividend payouts add up when you reinvest consistently—especially if you’re holding long-term.

Don’t Chase Hype

It’s tempting to jump into the latest hot ETF—AI, space, blockchain, you name it. But unless you’ve done the homework and believe in the long-term trend, be cautious. A lot of these niche funds are built to attract attention, not necessarily deliver returns.

Avoid investing just because something is trending online or had a big one-month return. FOMO is not a strategy.

Watch Out for Portfolio Overlap

It’s easy to think you’re diversified because you own several different ETFs—but many of them may hold the exact same companies. For example, if you own a tech ETF, an S&P 500 ETF, and a growth ETF, you probably have a lot of exposure to Apple, Microsoft, Amazon, and Google. Check the top holdings of your ETFs, and make sure you’re not unintentionally doubling or tripling your bets on the same names when you´re seeking a higher degree of diversification.

How to Invest in ETFs

Open a Brokerage Account: ETFs are bought and sold like stocks, so you’ll need a brokerage account. Many online brokers offer ETFs, and some even provide commission-free ETFs.

Choose Your ETF: Determine what you’re looking to invest in—whether it’s a broad market index, a specific sector, or a global economy. Consider the ETF’s expense ratio, liquidity, and performance relative to its benchmark.

Monitor and Rebalance: Once you’ve invested in an ETF, it’s important to periodically review its performance. You may need to rebalance your portfolio if your allocations shift over time.

Exchange-Traded Funds (ETFs) have become integral to modern investing, appealing to both individual and institutional investors. Their surge in popularity is largely due to their ability to offer versatility, tax efficiency, and cost-effectiveness, making them an attractive option within the vast global investment landscape. As we look to the future, several emerging trends and innovations are poised to reshape the ETF market significantly.

Technological Integration in ETF Management

Technological advancements are at the forefront of transforming the landscape of ETF management. The integration of modern technology is changing the methods by which ETFs are created, managed, and traded. Data analytics, artificial intelligence (AI), and blockchain technology are three critical areas driving this transformation, allowing fund managers to deploy sophisticated strategies with enhanced accuracy and efficiency.

Blockchain and Tokenization

One technological advancement providing promising developments is blockchain, which holds the potential to revolutionize ETFs in terms of transaction transparency and efficiency. By utilizing blockchain, settlement times can be significantly reduced, offering a more streamlined and cost-effective trading process. Additionally, tokenization is an emerging phenomenon that enables the digital representation of assets. This advancement might pave the way for increased diversity and fractionalized investment opportunities within the ETF market, offering more customized investment options and a broadening of potential asset classes.

Rise of Thematic and ESG ETFs

There is a growing investor interest in aligning portfolios with personal values and emerging global trends. This shift has spurred the rise of Thematic ETFs, which focus on particular themes or sectors such as technological innovations, biotech advancements, or renewable energy sources. These ETFs allow investors to target specific areas of economic growth or interest, reflecting a more tailored approach to investment.

Additionally, the focus on social responsibility in investing has been bolstered by Environment, Social, and Governance (ESG)-focused ETFs. As more investors prioritize sustainable practices, the influence of ESG principles continues to grow. Investors find these ETFs attractive as they seek to balance financial returns with social good, in keeping with broader societal shifts towards sustainability.

Customization and Direct Indexing

Technological advancements have also facilitated increased levels of customization within investment portfolios. The development of Direct Indexing is particularly noteworthy, offering investors the opportunity to create bespoke portfolios that simultaneously track a specific index while also being customizable based on individual tax preferences or personal values.

Smart Beta and Factor Investing

Among the innovative strategies in the ETF space, smart beta is gaining traction. Smart beta strategies aim to outperform traditional market-cap weighted indices through factor-based investing. Factors such as value, momentum, and low volatility have been popular choices among investors. By prioritizing these factors, smart beta ETFs allow investors to maintain a disciplined, rule-based approach to investing while seeking to achieve above-market returns.

Regulatory Changes and Challenges

In tandem with the evolving ETF market, regulatory frameworks are also in flux, adapting to the novel challenges and opportunities presented by this dynamic field. It remains critical for investors to track changes in regulations, as these can affect various aspects such as trading strategies, taxation, and overall operational frameworks of ETFs. Regulatory updates from securities commissions and other governing bodies worldwide are anticipated to play a decisive role in shaping the future of ETFs, influencing how these funds are structured and offered to the public.

Conclusion

Looking forward, the future of ETFs is positioned to be profoundly influenced by both technological advancements and regulatory developments, alongside an increasing demand for personalized and thematic investment options. Investors and financial advisors are encouraged to stay informed and responsive to these changes, thereby maximizing the potential to capitalize on opportunities while mitigating emerging risks. As these shifts continue to unfold, ETFs are anticipated to reinforce their standing as a central component of various investment strategies worldwide, offering lucrative pathways for diversified and efficient investing.

Understanding Expense Ratios and Fees in ETF Investing

Investing in Exchange-Traded Funds (ETFs) has become increasingly popular due to the benefits they offer such as diversification and potentially lower costs. Yet, a crucial part of making the most from ETF investments is an understanding of the cost structure that accompanies these financial instruments. Among the cost components that investors need to comprehend are the expense ratio and other related fees associated with ETF investing.

What is an Expense Ratio?

The expense ratio is a term that refers to the financial measurement of the cost required to manage and operate an ETF. Presented as a percentage of the fund’s average net assets, this expense is subtracted from the fund’s returns, directly affecting the investor’s earnings. The components of this ratio include management fees, administrative costs, and other operational expenses, and it serves as a broad gauge of the cost efficiency of an ETF. Generally speaking, a lower expense ratio suggests that a greater portion of the investment’s returns remains with the investor, making it a critical factor to consider when selecting among various ETFs.

Example of an Expense Ratio

To illustrate the impact of an expense ratio on an investment, consider an ETF with an expense ratio of 0.50%. This figure implies that for every $1,000 invested in the fund, $5 is expended annually to cover administrative costs and management fees. Thus, understanding this ratio is crucial as it determines how much of the fund’s returns are consumed by operational costs.

Components of the Expense Ratio

The expense ratio itself is composed of several cost elements:

Management Fees: These fees compensate fund managers for their expertise in investment decisions and their responsibility for handling the ETF’s portfolio. They can vary based on the investment strategy and complexity of the ETF.

Administrative Costs: Administrative expenses involve the essential services required for the smooth function of the ETF. These include tasks such as record-keeping, customer service, and other essential operational needs.

Marketing and Distribution Fees: Sometimes referred to as 12b-1 fees, these are intended to cover marketing and promotional activities aimed at increasing the ETF’s investor base. Importantly, not all ETFs charge these fees, but when they do, it adds to the total expense ratio.

Additional Fees to Consider

While the expense ratio is a key factor in assessing ETF costs, it is not the only cost component that investors should pay attention to. Several other fees can impact the total cost of investing in ETFs.

Brokerage Commissions

Most investors access ETFs through brokerage accounts, potentially incurring transaction fees or commissions. In recent years, many brokerage platforms have moved towards offering lower-cost or even commission-free trades. However, investors need to scrutinize these fees when deciding on where to buy or sell ETFs to ensure that transaction costs remain minimal.

Bid-Ask Spread

Another fee component is the bid-ask spread, which refers to the gap between the highest price a buyer is ready to pay for an ETF and the lowest price at which a seller is willing to sell. This difference can subtly affect the cost of trading ETFs, especially those that are less frequently traded and less liquid. Therefore, investors should take the bid-ask spread into account when calculating the total trade costs.

Comparing Costs Among ETFs

When evaluating potential ETF investments, investors should not only focus on the expense ratio but also consider other fees. While a lower expense ratio is typically more advantageous since it ensures more returns remain with the investor, it is equally important to evaluate the ETF’s overall performance, its investment strategy, and associated fees. This comprehensive analysis aids in making sound investment decisions.

Researching ETFs

Effective ETF research involves using dependable financial sources and analytical tools such as those offered by platforms like Morningstar and Vanguard. These resources provide detailed insights into a fund’s expense ratios and associated fees, helping investors perform a thorough analysis and make more informed investment decisions.

Conclusion

For those entering the realm of ETF investment, a clear understanding of expense ratios and the accompanying fees is vital. Awareness of the elements contributing to these costs coupled with considerations of additional charges ensures informed decision-making. By evaluating these components carefully, investors can position themselves to optimize their ETF investments, aligning their financial strategies with their long-term objectives. Ensuring that fees and costs don’t unnecessarily diminish returns is a strategic approach for achieving success in the dynamic world of ETF investing.

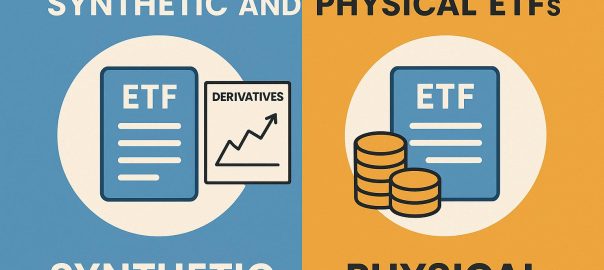

Exchange-traded funds (ETFs) have gained significant popularity as investment vehicles that offer individuals an accessible way to invest across a diversified portfolio of assets. However, it’s important for investors to recognize that not all ETFs operate in the same manner. The primary categories of ETFs, namely synthetic ETFs and physical ETFs, each bring their own sets of characteristics and implications for investors. A comprehensive understanding of the distinctions between these two types is crucial for making informed investment choices.

Physical ETFs: An Overview

Physical ETFs, often referred to as replicating ETFs, are constructed to directly emulate the performance of a particular index. This is achieved by holding the actual underlying assets that make up the index. For instance, consider a physical ETF that aims to track the S&P 500 index—this ETF will hold significant portions of shares from the 500 companies represented in the index. The replication of the index performance is generally achieved through methods like full replication or sampling. Full replication involves holding all the securities in the same proportions as the index, whereas sampling might involve holding a representative selection of the securities that make up the index.

Benefits of Physical ETFs

One of the substantial advantages of physical ETFs is their transparency. Investors have the benefit of easily accessing details about the actual securities they own because the ETF holds the real assets. This transparency fosters investor confidence as they can directly verify the ETF’s holdings.

Additionally, physical ETFs generally entail lower counterparty risk since the backing of the ETF is based on tangible assets. The investor’s risk mainly revolves around market risk rather than concerns about the solvency of a financial institution. This feature can be particularly appealing to investors who prioritize safety and asset-backed assurance in their investment portfolios.

Synthetic ETFs: An Overview

On the other end of the spectrum, synthetic ETFs do not hold the actual underlying assets associated with their target index. Instead, these ETFs rely on derivative products, with swaps being a common method to replicate the performance of an index. By using derivatives, synthetic ETFs can deliver returns consistent with the index through formal agreements with financial institutions. This method enables synthetic ETFs to track indices efficiently, even if the direct acquisition of the related securities would be impractical or prohibitively expensive.

Benefits and Risks of Synthetic ETFs

The notable advantage of synthetic ETFs is their capability to track indices that are difficult or costly to replicate physically. This often includes indices featuring illiquid securities or those representing emerging markets, where acquiring the underlying assets is challenging.

However, synthetic ETFs inherently carry a higher counterparty risk than their physical counterparts. This risk stems from their reliance on a financial institution’s ability to fulfill its contractual obligations. If the counterparty were to default, there could be financial repercussions for the ETF investors.

Counterparty Risk Management

To mitigate the higher counterparty risk, synthetic ETFs often use collateral arrangements. Typically, the involved financial institution is required to provide collateral that matches or exceeds the ETF’s exposure value. This collateral is maintained in a segregated account to offer a layer of protection for investors in the scenario of a counterparty failure. The effectiveness of these risk management strategies can be substantial, albeit not absolute, in safeguarding investors against counterparty insolvency.

Choosing Between Synthetic and Physical ETFs

Investors facing the decision of whether to opt for synthetic or physical ETFs must weigh several considerations. Such considerations include their personal risk tolerance, the specifics of the investment asset class, and the liquidity of the underlying index. A clear understanding of these factors is necessary in aligning investment actions with individual financial objectives and risk appetites.

Physical ETFs are often preferred for their clear and transparent nature, making them more attractive to investors who prioritize lower counterparty risk and straightforward asset verification. However, synthetic ETFs might present a more fitting solution for those seeking exposure to complex or less accessible markets that are not easily replicated through physical holdings.

It’s crucial for investors to conduct thorough research and seek insights from financial experts as necessary. Professional advice can be invaluable in determining which ETF type aligns best with an investor’s goals and risk profile. An adequate understanding of the nuances of each ETF type equips investors to make judicious decisions in the ever-expanding domain of exchange-traded funds.

For further insights, investors might consider exploring financial websites focused on investment strategies or engage with a financial advisor to deepen their understanding of ETFs and their potential roles in a diversified investment approach.

Dollar-cost averaging (DCA) is a systematic investment strategy that allows investors to consistently allocate a fixed sum of money into a particular investment, regardless of fluctuating market conditions. The crux of this method aims to minimize the risk associated with investing a lump sum amount at an inopportune moment when market conditions might be disadvantageous. This strategic approach is particularly useful in volatile markets where price variations are frequent, enabling investors to smoothen the effects of market ups and downs on their investments.

Benefits of Dollar-Cost Averaging

The primary advantage of dollar-cost averaging lies in its ability to reduce the impact of market volatility. By investing a set amount regularly, investors may purchase more shares when prices are low and fewer shares when prices are high, potentially resulting in a lower average cost per share over time. This tactic is particularly advantageous in unpredictable or highly volatile markets, where prices fluctuate frequently. Consequently, DCA offers a buffer against market volatility, safeguarding investors from the adverse effects of price swings, and can lead to beneficial outcomes over the long term.

Why Use ETFs?

Exchange-Traded Funds (ETFs) represent an optimal vehicle for implementing a dollar-cost averaging strategy. ETFs inherently offer diversification, as they invest in a diversified range of securities, which inherently mitigates risks compared to investing in individual stocks. Moreover, they are typically more cost-effective than certain mutual funds due to lower expense ratios. ETFs provide investors the opportunity to gain exposure to various asset classes or sectors without significant financial outlay, making them a preferred choice for many looking to leverage the benefits of DCA.

Implementing Dollar-Cost Averaging with ETFs

Investors interested in utilizing the dollar-cost averaging strategy with ETFs can follow a straightforward approach to get started. This involves a series of calculated steps designed to maximize returns while adhering to a disciplined investment routine.

Determine Your Investment Amount and Frequency

The first step in implementing DCA is to decide on the fixed amount to invest at regular intervals. This could be a modest sum such as $200 every month or every two weeks. The consistency of this investment is central to reaping the full benefits of DCA, as it ensures continuous participation in the market irrespective of its current state. This ongoing commitment can aid in building substantial investments over time.

Choose the Right ETFs

Subsequently, selecting the appropriate ETFs that align with one’s investment objectives and risk tolerance is pivotal. Investors should explore different categories of ETFs, such as those focusing on large-cap stocks, international markets, or specific industry sectors. The choice of ETFs should reflect the investor’s financial goals, time horizon, and comfort level with potential risks.

Set Up Automatic Investments

Automation is a key facet of successful DCA implementation, and many brokerage platforms offer features to set up automatic investments. This facility ensures that investments are systematically made in the chosen ETFs at predetermined intervals without requiring manual intervention. This not only aids in maintaining investment discipline but also eliminates the emotional biases that often affect investment decisions during market fluctuations.

Balancing Your Portfolio

Regular investment through DCA can contribute to maintaining a balanced portfolio over time. Investors should periodically review their portfolios to assess whether their ETF allocations are consistent with their broader investment strategy. Adjustments might be necessary to maintain the desired asset allocation, ensuring diversification and alignment with financial goals.

Risks and Considerations

Despite its advantages, dollar-cost averaging is not without potential downsides. In a market that consistently trends upwards, a lump-sum investment could potentially yield higher returns than a DCA approach, given the continuous rise in asset values. Additionally, the management fees associated with ETFs need to be considered, as they could impact overall returns. It is crucial for investors to weigh these considerations against the benefits of risk mitigation and peace of mind offered by DCA.

Tax Implications

The tax implications of regular investments should also be taken into account. Different tax rules may apply depending on whether investments are made in taxable or tax-advantaged accounts. These factors can affect the net returns realized from a dollar-cost averaging strategy, necessitating careful financial planning and possibly consultation with a tax advisor to optimize the strategy’s tax efficiency.

Final Thoughts

Adopting dollar-cost averaging with ETFs presents a well-rounded strategy for investors aiming to neutralize the adverse effects of market volatility. Through consistent investment over time, DCA can potentially optimize returns while offering the convenience of automated participation in the market. However, it remains imperative for investors to conduct comprehensive research or seek guidance from financial advisors to tailor a DCA approach that best suits their individual financial aspirations. By understanding the nuances of this strategy, investors can make informed decisions that contribute to achieving long-term financial security and growth.

In the world of investing, Exchange-Traded Funds (ETFs) have become increasingly popular due to their ability to offer diversification and liquidity. Among the various types of ETFs, Gold and Commodity ETFs hold a special place, particularly for those looking to protect their portfolios against inflation and market volatility. Understanding the nuances and strategic advantages of these investment vehicles can help investors make informed choices that align with their financial goals.

Understanding Gold and Commodity ETFs

Gold ETFs are investment funds that track the price of gold and are traded on stock exchanges just like shares. They offer investors a chance to gain exposure to the gold market without the need to physically own the metal. This feature makes Gold ETFs an attractive choice for investors seeking liquidity and ease of trading as they provide a hassle-free alternative to purchasing and storing physical gold.

On the other hand, Commodity ETFs invest in a range of primary resources or raw materials, including metals, agriculture, and energy. These ETFs can track the performance of a single commodity or a basket of various commodities, providing a means for investors to diversify their exposure to these markets. The choice between single-commodity ETFs and diversified ETFs depends on the investor’s risk tolerance and investment goals.

The Historical Role of Gold in Portfolio Protection

Gold has long been viewed as a safe haven asset. Traditionally, it has been used by investors to hedge against inflation, currency devaluation, and geopolitical uncertainty. The reason is that gold prices often move inversely to stocks and bonds; when the latter two decline in value, gold tends to increase or remain stable, thereby preserving wealth. Over the centuries, gold has maintained its allure as a store of value, offering a sense of security in tumultuous times. This historical perspective is vital for understanding why many investors still consider gold a crucial component of their portfolios not just as a source of returns, but more importantly, as a protector of purchasing power.

Commodity ETFs: A Broader Scope

While gold offers specific advantages, Commodity ETFs provide a broader scope for protection. For instance, energy commodities like oil can hedge against inflation driven by rising fuel costs. Agricultural commodity ETFs can protect against food price inflation. These ETFs enable diversification beyond gold, thereby spreading risk across different segments of the economy. The ability to invest in a combination of commodities can potentially reduce volatility that might be more prevalent in single commodity investments, allowing investors to position their portfolios in alignment with broader economic trends and cycles.

Benefits of Including Gold and Commodity ETFs in a Portfolio

Protection Against Inflation: Both Gold and Commodity ETFs are known for their inflation-hedging abilities. As inflation rises, the cost of raw materials and commodities typically increases, potentially boosting the value of these ETFs. This feature makes them a natural choice for investors concerned about preserving purchasing power in a rising cost environment.

Diversification: By adding Gold and Commodity ETFs, investors can diversify their portfolios, reducing the risk associated with relying solely on equities or bonds. Diversification helps smooth out the performance of a portfolio over time, as different asset classes react differently to economic, political, and market events.

Liquidity: Unlike physical commodities, ETFs can be easily bought and sold on exchanges, offering investors flexibility and ease of transaction. This feature is particularly beneficial during times of market distress when quick access to cash might be needed.

Global Exposure: Commodity ETFs offer exposure to a variety of global markets, which can be beneficial in capitalizing on growth trends in different regions around the world. This global reach allows investors to tap into markets that are poised for growth due to economic development or demographic trends.

Risks and Considerations

While Gold and Commodity ETFs provide numerous advantages, they are not free from risks. Market volatility, geopolitical changes, and shifts in global demand and supply can all impact their performance. Investors should consider these factors and align their investments with their risk tolerance and financial goals. Additionally, commodity prices can be highly volatile, affected by factors such as weather, political instability, and technological innovations, which can introduce significant variability in the returns of Commodity ETFs.

Tax Implications

Investors should also be aware of the tax implications associated with these ETFs. In some jurisdictions, profits from Gold ETFs might be subject to different tax rates than other investments. It is advisable to consult with a tax professional to understand the specific tax obligations. The tax treatment of ETF investments can vary significantly depending on factors like the investor’s country of residence, the structure of the ETF, and the tax classification of the underlying assets. Understanding these nuances is crucial for optimizing after-tax returns.

Conclusion

Gold and Commodity ETFs serve a vital role in portfolio protection by offering inflation hedging, diversification, and the potential for reduced volatility. While they should not be viewed as a panacea for all investment risks, when used strategically, they can enhance the overall resilience and performance of an investment portfolio. As always, prospective investors should perform due diligence and consider their financial objectives before proceeding. Effective utilization of these instruments entails not only understanding their advantages but also recognizing their limitations within the broader context of a diversified investment strategy.

For further reading on integrating ETFs into your investment strategy, consult this comprehensive guide on ETFs.

Understanding Currency Hedged ETFs in International Investing

In today’s global market, investors seek opportunities beyond their domestic borders, targeting international markets for diversification and growth potential. However, venturing into foreign markets introduces unique challenges, notably currency risk, which is the risk that changes in exchange rates could impact the return on investments. Currency Hedged Exchange Traded Funds (ETFs) have emerged as an effective tool to address this challenge, allowing investors to concentrate more on the performance of equity markets rather than the fluctuations in currency values.

What Are Currency Hedged ETFs?

Currency Hedged ETFs are specialized investment vehicles designed to minimize or eliminate the impact of currency movements on investment returns. This is achieved through strategic use of financial instruments such as futures or forwards, which are contracts to buy or sell an asset at a predetermined future date and price. By implementing these mechanisms, Currency Hedged ETFs provide investors with an opportunity to participate in international markets but view their returns from a perspective that is isolated from currency market volatility. Therefore, the primary focus remains on the performance of the held assets, such as stocks, without currency fluctuations skewing the investment outcome.

Mechanics of Currency Hedging

At the core of Currency Hedged ETFs lies a strategy aimed specifically at managing currency risk. Typically, these ETFs adopt an opposite position in the foreign exchange (FX) market to balance the currency exposure inherent in the ETF’s holdings. For instance, consider an ETF investing in European equities. If the euro depreciates against the dollar, an unhedged position would lead to decreased returns due to the currency devaluation. In contrast, a Currency Hedged ETF would use hedging strategies, like short positions in currency futures, to counterbalance any losses stemming from the currency decline, ensuring that the investor’s returns remain primarily contingent on the performance of the European stocks themselves.

Benefits of Using Currency Hedged ETFs

There are notable advantages to incorporating Currency Hedged ETFs into an investment portfolio, driven by their designed benefits:

Mitigation of Currency Risk: The primary advantage of Currency Hedged ETFs is their ability to neutralize the effect of currency volatility, thereby preserving the integrity of returns derived from international investments. This stability allows investors to focus on the core performance metrics of their chosen assets.

Focused Asset Performance: Without the distraction of currency fluctuations, investors can better analyze the intrinsic performance of the underlying assets, be it equities, bonds, or other instruments. This clarity in evaluation aids in making informed investment decisions.

Portfolio Diversification: Despite shielding returns from currency movements, Currency Hedged ETFs contribute significantly to diversifying a portfolio. They offer exposure to global markets while maintaining a domestic currency viewpoint, enabling investors to capitalize on geographic and sectoral diversification.

Potential Drawbacks

While these ETFs bring several benefits, potential drawbacks exist that must be carefully considered:

Costs: The implementation of currency hedging adds complexities and, consequently, additional costs. These include higher transaction fees and expense ratios compared to non-hedged ETFs, which could slightly eat into the overall returns.

Performance Drag: A secondary risk involves the possibility that the foreign currency strengthens. In such instances, a hedged position may preclude investors from enjoying an enhanced return provided by the appreciated currency against their domestic counterpart.

How to Invest in Currency Hedged ETFs

To effectively incorporate Currency Hedged ETFs into an investment strategy, investors can follow several key steps:

– Assess risk tolerance and align it with their long-term investment goals. Understanding personal appetite for risk and the role currency exposure plays in the investment strategy is crucial.

– Consider the economic outlook for the currencies involved. Analyzing the predicted performance of both the domestic and foreign currencies helps decide if hedging is warranted.

– Conduct thorough research on ETFs, inspecting factors such as expense ratios, issuers, and liquidity profiles. Not all Currency Hedged ETFs are created equal, and understanding these nuances ensures alignment with investment objectives.

Seeking advice from a financial advisor can vastly enhance the understanding and decision-making process, providing insights tailored to individual circumstances. Financial experts can assist in fine-tuning strategies that effectively incorporate Currency Hedged ETFs, ensuring they complement existing portfolio objectives.

By leveraging the potential of Currency Hedged ETFs, investors position themselves to better navigate the challenges posed by international markets. With a comprehensive grasp of these financial instruments, investors can adeptly protect themselves from currency risk, focusing confidently on gauging and optimizing the performance of their international assets. By focusing on the fundamentals of investments and bolstering portfolios against adverse currency movements, investors can confidently pursue opportunities that global markets present.

The Impact of Market Volatility on ETF Performance

Exchange-traded funds (ETFs) have emerged as highly favored investment vehicles in recent decades. They offer a compelling blend of benefits, primarily due to their ability to provide diversification coupled with typically lower fees compared to traditional mutual funds. For investors keen on maximizing their investment outcomes, it is crucial to delve into how ETFs perform under varying market conditions. This understanding becomes especially significant during periods marked by market volatility, which often introduces additional complexity and risk.

Market Volatility Defined

Market volatility can be best described as the pace at which securities’ prices in the market either surge upward or plummet downward relative to a given set of returns. A commonly used metric to quantify this volatility is the standard deviation of returns, which essentially measures the extent of variation or dispersion of a set of financial data points. A rising tide of volatility is often synonymous with increased uncertainty and risk from the perspective of investors. These conditions can lead to substantial fluctuations in the performance of ETFs, making it imperative for investors to consider how volatility can influence their investment strategy.

Factors Influencing ETF Performance

When assessing ETF performance, particularly during times of elevated market volatility, several interconnected factors come into play:

Underlying Index: A salient characteristic of most ETFs is their objective to mirror the performance of an underlying index. As such, the volatility inherent in the index itself has a direct bearing on an ETF’s performance. For instance, indices that concentrate on specific sectors like technology or on emerging markets tend to witness increased volatility compared to more diversified or established market indices. Therefore, the choice of index plays a critical role in determining the ETF’s response to market dynamics.

Liquidity: The liquidity of an ETF is a crucial determinant of how easily and efficiently investors can buy or sell shares without substantially impacting the price. During volatile market periods, liquidity can be compromised, resulting in wider bid-ask spreads. This situation renders trading in ETFs more expensive and less predictable during turbulent phases, affecting overall investment strategies and decisions.

Tracking Error: This concept refers to the divergence between the performance of an ETF and its intended target index. In an environment of increased volatility, the tracking error might widen, primarily because ETF managers face challenges in precisely mirroring the rapid fluctuations of the index. Influencing factors may include transaction costs, differences in timing, and other operational constraints that complicate the replication process.

Benefits of ETFs in Volatile Markets

Despite the potential pitfalls, ETFs leverage several inherent advantages that can be capitalized on during volatile market conditions:

Diversification: By investing in ETFs, individuals gain access to a broad spectrum of assets, industries, or regions, effectively spreading risk across a multitude of holdings. In times of volatility, this diversification acts as a stabilizing factor, helping to manage and mitigate risk by not placing all financial resources in a singular or narrow investment path.

Cost-Effectiveness: ETFs generally present lower expense ratios compared to actively managed funds. This cost-efficiency serves as a particularly valuable advantage during uncertain market scenarios when every basis point gained or saved translates into meaningful financial benefit. As markets turn precarious, the lower costs associated with ETFs may contribute positively to investors’ overall returns.

Flexibility: The ability to trade ETFs on stock exchanges in the same manner as individual stocks provides investors with a level of transactional flexibility that is highly prized in rapidly changing markets. This feature allows investors to make real-time decisions and execute transactions throughout the trading day, thereby offering agility and responsiveness to fluid market developments.

Strategies to Mitigate Risk

For investors keen on navigating the inherent risks associated with market volatility while investing in ETFs, several strategic approaches can be deployed:

Focus on Low-Volatility ETFs: Certain ETFs are purposefully designed to provide exposure to stocks characterized by low volatility. These assets are often seen as more stable and less susceptible to abrupt price swings during periods of market instability. Such ETFs usually concentrate on companies that exhibit steady earnings profiles and possess a historical track record of less dramatic price movements.

Diversify Across Asset Classes: Embracing diversification across different asset classes such as equities, bonds, and commodities through a mix of ETFs can significantly reduce portfolio volatility. By spreading investment across varied asset classes, investors can balance risk and harness the advantage of multiple income streams and growth opportunities.

Monitor Economic Indicators: Economic indicators serve as valuable tools in evaluating potential market movements. By keeping a close watch on key economic metrics like interest rates, GDP growth, and employment figures, investors can make informed assessments of market dynamics and accordingly adjust their ETF portfolios. This proactive monitoring aids in aligning investment strategies with prevailing economic conditions.

Conclusion

While market volatility naturally presents challenges for ETF performance, a deep understanding of the underlying factors influencing it and the adoption of strategic investment approaches can aid investors in harnessing the intrinsic advantages of ETFs. A well-rounded strategy that capitalizes on diversification and cost-effectiveness can position investors to effectively navigate volatile markets and optimize their portfolios for the long term. For further insights into the workings of ETFs and related investment strategies, individuals are encouraged to explore comprehensive resources such as those available on Investopedia. This will equip investors with the knowledge necessary to make informed decisions in an ever-evolving financial landscape.

Smart Beta Exchange-Traded Funds (ETFs) have emerged as a noteworthy investment strategy, offering a synthesis of traditional index investing complemented by elements of active portfolio management. This investment approach differentiates itself from conventional strategies that are typically governed by market capitalization-weighted indices. By adopting a non-traditional framework, Smart Beta ETFs aim to enhance returns, improve diversification, and potentially mitigate risk.

What Makes Smart Beta Different?

In a traditional index fund setup, investments are typically allocated based on market capitalization, which implies proportionate representation to the market value of the stocks. In stark contrast, Smart Beta ETFs adopt a distinctive methodology by selecting and weighting investments based on certain predetermined factors or rules. Key factors often emphasized include volatility, momentum, quality, value, and size. These specific criteria strive to encapsulate the advantageous characteristics associated with active management, such as the pursuit of higher returns and better risk management. Simultaneously, Smart Beta ETFs uphold the benefits usually associated with index funds, namely cost-effectiveness and transparency.

Key Characteristics of Smart Beta Funds

Factor-Based Investing: A fundamental attribute of Smart Beta ETFs is their orientation towards factor-based investing. This strategy seeks to harness systematic factors like volatility, momentum, or size. Through this differentiation, Smart Beta ETFs provide an alternative approach compared to merely tracking indices based on market capitalization.

Rules-Based Approach: The selection and weighting processes in these funds are primarily rules-based, contributing to transparency and consistency over time. The adherence to a rules-based method ensures that the fund aligns with its predetermined investment criteria, consequently minimizing subjective human biases which could affect decision-making.

Cost-Effective: While Smart Beta ETFs generally incur higher expenses than traditional index funds, they remain relatively more affordable than actively managed funds. For investors aiming to amplify returns while keeping costs manageable, this cost-effectiveness presents an enticing opportunity.

How Do Smart Beta ETFs Work?

Central to the functioning of Smart Beta ETFs is a well-defined set of rules guiding stock selection. Consider a Smart Beta ETF dedicated to low volatility; such a fund would prioritize stocks that have historically displayed stability, offering a buffer during periods of market downturns. On the other hand, a fund focusing on high dividend yields would target stocks with a proven history of rewarding shareholders through dividends.

Each Smart Beta ETF is anchored by a meticulously defined strategy, articulated in the fund’s prospectus. This critical document sheds light on the selection criteria and provides clarity on the factors that the fund emphasizes. Prospective investors considering Smart Beta ETFs should carefully evaluate the alignment of these factors with their individual financial aspirations and outlooks on market conditions.

Advantages and Disadvantages

Smart Beta ETFs offer several potential advantages. For instance, they may offer improved risk-adjusted returns and enhanced diversification, positioning them as attractive options for diversified portfolio construction. However, alongside these benefits, there are notable concerns. A key limitation is their dependence on historical data for factor selection—a reliance that poses risks as past performance does not invariably predict future outcomes. Furthermore, the complexity involved in understanding such strategies, as opposed to more straightforward traditional index funds, can be an impediment for some investors.

Choosing the Right Smart Beta ETF

Integrating Smart Beta ETFs into an investment portfolio warrants careful consideration and thorough research. Investors should take into account their unique risk tolerance levels and investment objectives. Examining aspects like historical performance, fee structures, and the reputation of the ETF provider is essential when making informed decisions. Additionally, seeking advice from a financial advisor could provide beneficial, tailored insights and guidance in navigating the selection of Smart Beta ETFs.